Here is a more analytical approach.

We want to find $E(Z)$ where

$$Z=X_1/\sum_{i=1}^n X_i=X_1/ \left(X_1+\sum_{i=2}^n X_i\right)=X_1/(X_1+Y)$$

where the $X_i$ random variables are independent exponential distributions all with different parameters:

$$X_i \sim \text{Exponential}(\lambda_i)$$

and $Y$ has a hypoexponential distribution with parameters $\lambda_2, \ldots,\lambda_n$.

The pdf of $Y$ is

$$\left(\prod_{i=2}^n \lambda_i\right) \sum_{i=2}^n \left(e^{-y \lambda_i} /\prod_{\substack{j=2 \\j\neq i}}^n {(\lambda_j-\lambda_i)}\right)$$

The mean of $Z$ can be found with the following:

$$\mu=\int_0^\infty \int_0^\infty \frac{x_1}{x_1+y} e^{-x_1 \lambda_1} \lambda_1 \left(\prod_{i=2}^n \lambda_i\right) \sum_{i=2}^n \left(e^{-y \lambda_i}/ \prod_{\substack{j=2 \\j\neq i}}^n {(\lambda_j-\lambda_i)}\right) dy dx_1$$

$$=\left(\prod_{i=1}^n \lambda_i\right) \sum_{i=2}^n

\frac{1}{\prod_{\substack{j=2 \\j\neq i}}^n {(\lambda_j-\lambda_i)}} \int_0^\infty \int_0^\infty \frac{x_1}{x_1+y} e^{-x_1 \lambda_1-y \lambda_i} dy \ dx_1$$

$$= \left(\prod_{i=1}^n \lambda_i\right) \sum_{i=2}^n

\frac{1}{\prod_{\substack{j=2 \\j\neq i}}^n {(\lambda_j-\lambda_i)}} \frac{\lambda_i-\lambda_1 (1+\log(\lambda_i/\lambda_1))}{\lambda_1(\lambda_1-\lambda_i)^2}$$

Addition

To answer the comment: Find the mean when the first $k$ $\lambda$'s are not equal but the last $n-k$ $\lambda$'s are all equal to $\mu_{k+1}$ which doesn't equal any of the first $k$ $\lambda$'s.

I have no desire to perform the needed algebra by hand so I'm using Mathematica as in my other answer.

(* Set values for n and k *)

n = 6;

k = 3;

(* Obtain mean when no lambdas are equal *)

μ = Product[λ[i], {i, 1, n}] Sum[(λ[i] - λ[1] (1 + Log[λ[i]/[1]]))/

(Product[If[j == i, 1, λ[j] - λ[i]], {j, 2, n}] λ[1] (λ[1] - λ[i])^2), {i, 2, n}];

(* Take the limit of μ as λ[k+1],...,λ[n] -> m = λ[k+1] *)

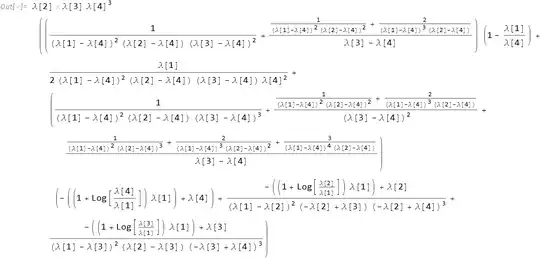

μ = (Limit[μ, Table[λ[i] -> m, {i, k + 1, n}]]) /. m -> λ[k + 1]

As a check set some $\lambda$ values and perform some simulations:

lambdas = {1, 2, 3, 4, 4, 4};

μ /. Table[λ[i] -> lambdas[[i]], {i, 1, k + 1}] // N]

(* 0.341686 *)

SeedRandom[12345]

nSims = 10000000;

(* Random samples from n exponentials )

data = Transpose[Table[RandomVariate[ExponentialDistribution[lambdas[[i]]], nSims],

{i, 1, n}]];

( Find x[1]/(x[1]+...+x[n] for each simulation )

z = #[[1]]/Total[#] & /@ data;

( Mean of simulated z values )

Mean[z]

( 0.341589 *)

2nd addition

If you have any of the $\lambda$ values that are equal, then probably the more efficient way to obtain the associated mean (that also doesn't require one to take limits) is to use @RiverLi 's answer with Mathematica (or Maple or MATLAB). Here is a Mathematica implementation of that:

λ = {3, 2, 5, 5, 5}

Integrate[(λ[[1]]/(s + λ[[1]])^2) Product[λ[[i]]/(s + λ[[i]]), {i, 2, Length[λ]}],

{s, 0, ∞}, Assumptions -> Table[λ[[i]] > 0, {i, 1, Length[λ]}]]

(* -(5/72) (708 + 400 Log[2] + 675 Log[3] - 1075 Log[5]) *)

That code also works symbolically:

λ = {λ1, λ2, λ3, λ3, λ3};

Integrate[(λ[[1]]/(s + λ[[1]])^2) Product[λ[[i]]/(s + λ[[i]]), {i, 2, Length[λ]}],

{s, 0, ∞}, Assumptions -> Table[λ[[i]] > 0, {i, 1, Length[λ]}]]